[ad_1]

The global auto industry continues to navigate a challenging

supply chain environment as well as lingering COVID-19 impacts.

While ongoing COVID lockdowns in areas of mainland China are having

a material impact on production within the country and some

surrounding markets, S&P Global Mobility (formerly IHS Markit |

Automotive) analysts are also seeing a measure of stability in

other regions relative to some of the more meaningful downward

revisions made in recent months.

To be sure, COVID conditions and the general state of the supply

chain will remain dominant factors influencing production in the

near-term, along with the macro implications of the ongoing

Russia/Ukraine conflict, yet automakers and suppliers continue to

adapt to the changing landscape.

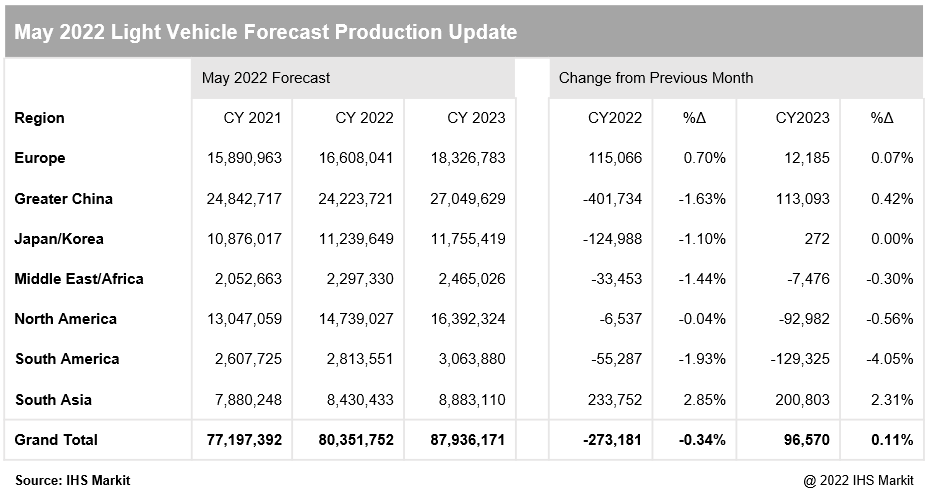

The May 2022 light vehicle production forecast update from

S&P Global Mobility reflects noteworthy reductions for Greater

China and Japan/Korea due to the aforementioned COVID lockdowns in

China impacting production both directly and through supply chain

interruptions. Conversely, it is important to note upward revisions

for South Asia and Europe on somewhat improved conditions in those

markets relative to prior expectations.

This article was published by S&P Global Mobility and not by S&P Global Ratings, which is a separately managed division of S&P Global.

[ad_2]

Source link